")

How do Monopolistic Competitors Affect Market Entry?

If one monopolistic competitor earns positive economic profits, other firms will be tempted to enter the market.

The entry of other firms into the same general market shifts the demand curve that a monopolistically competitive firm faces. As more firms enter the market, the quantity demanded at a given price for any particular firm will decline, and the firm’s perceived demand curve will shift to the left.

As a firm’s perceived demand curve shifts to the left, its marginal revenue curve will shift to the left, too. The shift in marginal revenue will change the profit-maximizing quantity that the firm chooses to produce, since marginal revenue will then equal marginal cost at a lower quantity.

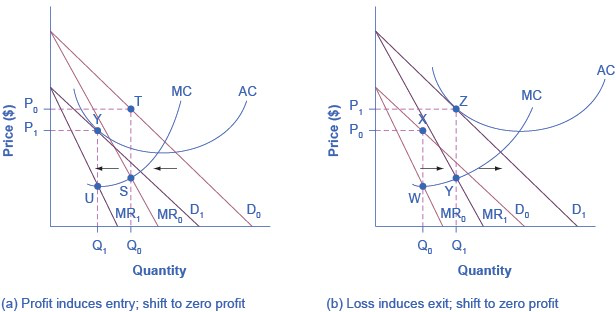

(a) At P0 and Q0, the monopolistically competitive firm in this figure is making a positive economic profit. This is clear because if you follow the dotted line above Q0, you can see that price is above average cost. Positive economic profits attract competing firms to the industry, driving the original firm’s demand down to D1. At the new equilibrium quantity (P1, Q1), the original firm is earning zero economic profits, and entry into the industry ceases. In (b) the opposite occurs. At P0 and Q0, the firm is losing money. If you follow the dotted line above Q0, you can see that average cost is above price. Losses induce firms to leave the industry. When they do, demand for the original firm rises to D1, where once again the firm is earning zero economic profit.

Unlike a monopoly, with its high barriers to entry, a monopolistically competitive firm with positive economic profits will attract competition. When another competitor enters the market, the original firm’s perceived demand curve shifts to the left, from D0 to D1, and the associated marginal revenue curve shifts from MR0 to MR1. The new profit- maximizing output is Q1, because the intersection of the MR1 and MC now occurs at point U. Moving vertically up from that quantity on the new demand curve, the optimal price is at P1.

As long as the firm is earning positive economic profits, new competitors will continue to enter the market, reducing the original firm’s demand and marginal revenue curves. The long-run equilibrium is in the figure at point Y, where the firm’s perceived demand curve touches the average cost curve. When price is equal to average cost, economic profits are zero. Thus, although a monopolistically competitive firm may earn positive economic profits in the short term, the process of new entry will drive down economic profits to zero in the long run. Remember that zero economic profit is not equivalent to zero accounting profit.

A zero economic profit means the firm’s accounting profit is equal to what its resources could earn in their next best use.

The economic losses lead to firms exiting, which will result in increased demand for this particular firm, and consequently lower losses. Firms exit up to the point where there are no more losses in this market, for example when the demand curve touches the average cost curve, as in point Z.

Monopolistic competitors can make an economic profit or loss in the short run, but in the long run, entry and exit will drive these firms toward a zero economic profit outcome. However, the zero economic profit outcome in monopolistic competition looks different from the zero economic profit outcome in perfect competition in several ways relating both to efficiency and to variety in the market.