")

What are Menu Costs?

These costs of changing prices are called menu costs—like the costs of printing a new set of menus with different prices in a restaurant. Prices do respond to forces of supply and demand, but from a macroeconomic perspective, the process of changing all prices throughout the economy takes time.

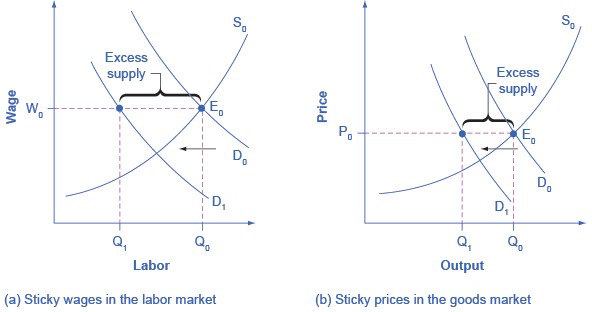

To understand the effect of sticky wages and prices in the economy, (a) illustrating the overall labor market (b) illustrates a market for a specific good or service. The original equilibrium (E0) in each market occurs at the intersection of the demand curve (D0) and supply curve (S0). When aggregate demand declines, the demand for labor shifts to the left (to D1). And the demand for goods shifts to the left (to D1) . However, because of sticky wages and prices, the wage remains at its original level (W0) for a period of time and the price remains at its original level (P0).

As a result, a situation of excess supply—where the quantity supplied exceeds the quantity demanded at the existing wage or price—exists in markets for both labor and goods, and Q1 is less than Q0. When many labor markets and many goods markets all across the economy find themselves in this position, the economy is in a recession; that is, firms cannot sell what they wish to produce at the existing market price and do not wish to hire all who are willing to work at the existing market wage. The Clear It Up feature discusses this problem in more detail.

In both (a) and (b), demand shifts left from D0 to D1. However, the wage in (a) and the price in (b) do not immediately decline. In (a), the quantity demanded of labor at the original wage (W0) is Q0, but with the new demand curve for labor (D1), it will be Q1.

Similarly, in (b), the quantity demanded of goods at the original price (P0) is Q0, but at the new demand curve (D1) it will be Q1. An excess supply of labor will exist, which we call unemployment. An excess supply of goods will also exist, where the quantity demanded is substantially less than the quantity supplied. Thus, sticky wages and sticky prices, combined with a drop in demand, bring about unemployment and recession.