Long Run Average Cost and Industry Competitors

Written by J. Mance Gordon

Updated at April 23rd, 2024

- Marketing, Advertising, Sales & PR

- Accounting, Taxation, and Reporting

- Professionalism & Career Development

-

Law, Transactions, & Risk Management

Government, Legal System, Administrative Law, & Constitutional Law Legal Disputes - Civil & Criminal Law Agency Law HR, Employment, Labor, & Discrimination Business Entities, Corporate Governance & Ownership Business Transactions, Antitrust, & Securities Law Real Estate, Personal, & Intellectual Property Commercial Law: Contract, Payments, Security Interests, & Bankruptcy Consumer Protection Insurance & Risk Management Immigration Law Environmental Protection Law Inheritance, Estates, and Trusts

- Business Management & Operations

- Economics, Finance, & Analytics

How does the Long-Run Average Cost Curve Affect Industry Competitors?

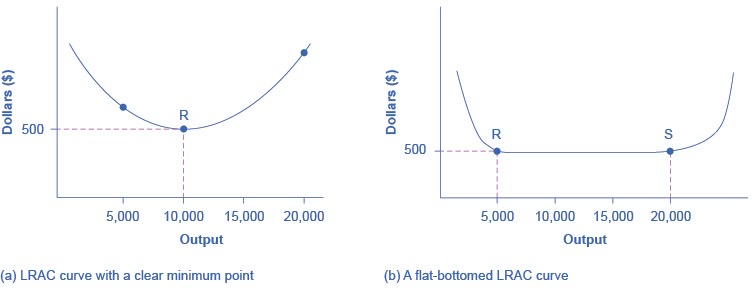

The shape of the long-run average cost curve affects the size and number of firms that will compete in an industry.

Where the LRAC curve has a flat-bottomed area of constant returns to scale.

If the LRAC curve has a single point at the bottom, then the firms in the market will be about the same size, but if the LRAC curve has a flat-bottomed segment of constant returns to scale, then firms in the market may be a variety of different sizes.

The relationship between the quantity at the minimum of the long-run average cost curve and the quantity demanded in the market at that price will predict how much competition is likely to exist in the market.

If the quantity demanded in the market far exceeds the quantity at the minimum of the LRAC, then many firms will compete. If the quantity demanded in the market is only slightly higher than the quantity at the minimum of the LRAC, a few firms will compete. If the quantity demanded in the market is less than the quantity at the minimum of the LRAC, a single- producer monopoly is a likely outcome.

Relate Topics

- Theory of the Firm

- Capital Formation

- Rent Seeking

- Structure Conduct Performance Model

- Integration

- Co-Insurance Effect

- Conglomerates

- Cost vs Profit Center

- Accelerator Theory

- Market Structure

- Fixed Cost vs Variable Cost

- Actual vs Implicit Costs

- Explicit Costs

- True Cost Economics

- Accounting Profit

- Economic Profit

- What are Factors of Production?

- Factor Income

- Production Function

- Fixed and Variable Inputs

- Short-Run and Long-Run Production

- Short Run

- Total Product

- Marginal Product

- Value of Marginal Product

- Law of Marginal Diminishing Product

- Production Function

- Production Possibilities Frontier

- Capital

- Labor Theory of Value

- How the Production Function Estimates Inputs

- Factor Payment

- Economic Rent

- Cost Function

- Incremental Cost

- Marginal Input Cost

- Fixed and Variable Costs

- Diminishing Marginal Productivity

- Costs Relate to Diminishing Marginal Productivity

- Law of Diminishing Marginal Returns

- Average Total Cost

- Average Variable Cost

- Marginal Cost

- Average Profit or Profit Margin

- Accounting Profit

- Economic Profit

- Normal Profit

- Short and Long-Run Production

- Cost Curves

- Long-Run Average Cost (LRAC)

- Production Technologies

- Economies of Scope

- Economies of Scale

- Diseconomies of Scale

- Minimum Efficient Scale

- Increasing, Constant, and Decreasing Returns to Scale

- Shape of the Average Long-Run and Short-Run Cost Curves

- Returns to Scale

- Diseconomies of Scale

- Long-Run Average Cost Curve Affect Industry Competitors

- Technology Shifts the Long-Run Average Cost Curve

- Law of Diminishing Marginal Returns