")

What is the Keynesian Approach to Unemployment and Inflation?

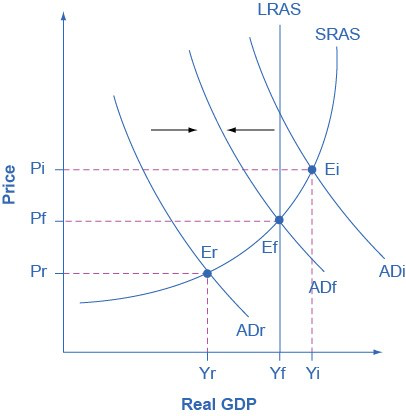

Keynesian macroeconomics argues that the solution to a recession is expansionary fiscal policy, such as tax cuts to stimulate consumption and investment, or direct increases in government spending that would shift the aggregate demand curve to the right. For example, if aggregate demand was originally at ADr, so that the economy was in recession, the appropriate policy would be for government to shift aggregate demand to the right from ADr to ADf, where the economy would be at potential GDP and full employment.

Keynes noted that while it would be nice if the government could spend additional money on housing, roads, and other amenities, he also argued that if the government could not agree on how to spend money in practical ways, then it could spend in impractical ways. For example, Keynes suggested building monuments, like a modern equivalent of the Egyptian pyramids. He proposed that the government could bury money underground, and let mining companies start digging up the money again. These suggestions were slightly tongue-in-cheek, but their purpose was to emphasize that a Great Depression is no time to quibble over the specifics of government spending programs and tax cuts when the goal should be to pump up aggregate demand by enough to lift the economy to potential GDP.

If an economy is in recession, with an equilibrium at Er, then the Keynesian response would be to enact a policy to shift aggregate demand to the right from ADr toward ADf. If an economy is experiencing inflationary pressures with an equilibrium at Ei, then the Keynesian response would be to enact a policy response to shift aggregate demand to the left, from ADi toward ADf.

The other side of Keynesian policy occurs when the economy is operating above potential GDP. In this situation, unemployment is low, but inflationary rises in the price level are a concern. The Keynesian response would be contractionary fiscal policy, using tax increases or government spending cuts to shift AD to the left. The result would be downward pressure on the price level, but very little reduction in output or very little rise in unemployment. If aggregate demand was originally at ADi, so that the economy was experiencing inflationary rises in the price level, the appropriate policy would be for government to shift aggregate demand to the left, from ADi toward ADf, which reduces the pressure for a higher price level while the economy remains at full employment.

In the Keynesian economic model, too little aggregate demand brings unemployment and too much brings inflation. Thus, you can think of Keynesian economics as pursuing a “Goldilocks” level of aggregate demand: not too much, not too little, but looking for what is just right.